In the week beginning September 22, 2025, financial markets will closely monitor flash Purchasing Managers’ Index (PMI) data for early insights into global economic momentum, labor conditions, and inflation trends. A key highlight will be Friday’s release of the U.S. core Personal Consumption Expenditures (PCE) price index, the Federal Reserve’s preferred inflation gauge. Additional data to watch include revised second-quarter U.S. GDP figures, consumer sentiment indicators from the U.S. and Europe, existing and new home sales, durable goods orders, and inventory levels in the United States.

The initial PMI readings will offer the first comprehensive look at economic performance in September. Earlier reports indicated strong expansion in India, with solid growth also seen in the U.S. and Australia. Moderate but improving activity was recorded in the UK and Japan, while the eurozone showed more limited gains. Analysts are assessing whether recent manufacturing gains—partly driven by提前 shipments ahead of anticipated U.S. tariffs—are sustainable or fading. Attention will also focus on whether rising domestic demand in countries like Germany can counterbalance trade-related pressures. In France, the data may reflect economic repercussions following the collapse of the government, while in the UK, surveys will help evaluate the impact of higher employer taxes and minimum wage adjustments on inflation and employment. These policy shifts have contributed to inflationary pressures and notable job reductions across sectors.

In the U.S., while current output indicators suggest continued solid economic growth in the third quarter, business sentiment about the future has weakened, signaling growing corporate caution. Market participants will also scrutinize U.S. PMI price components to assess tariff-related inflationary effects. The upcoming core PCE data will be critical in shaping expectations for future monetary policy. Recent mixed signals—consumer prices rising from 2.7% to 2.9% in August, while wholesale prices unexpectedly fell by 0.1%—underscore the uncertainty. A softer inflation print may be necessary to justify additional rate cuts in the coming months. The Federal Open Market Committee’s last meeting included a rate reduction, the first since December, with officials projecting two more cuts by year-end, reflecting a more accommodative stance than previously expected.

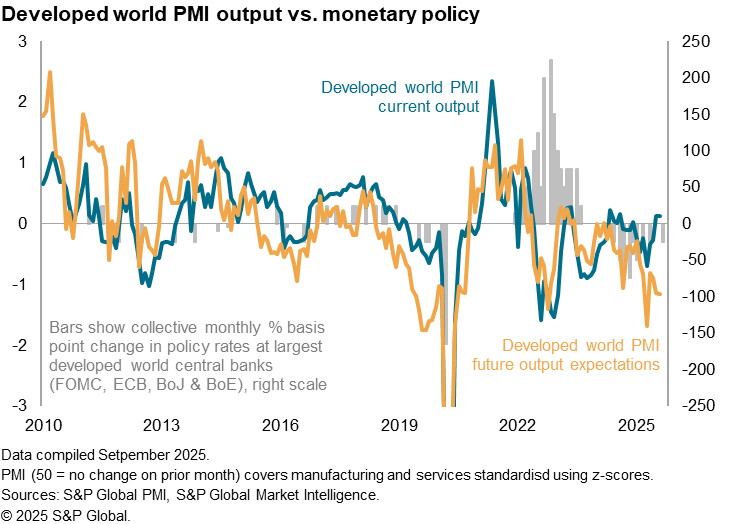

The divergence between strengthening current output and weakening forward-looking confidence is unusual and raises concerns about potential downside risks to the economic outlook. Key releases during the week include Canada’s Producer Price Index and Chicago Fed National Activity Index on Monday; flash PMI data for Australia, India, the UK, Germany, France, the eurozone, and the U.S. on Tuesday; Japan’s flash PMI on Wednesday; final U.S. GDP, durable goods orders, jobless claims, and wholesale inventories on Thursday; and core PCE, personal income, spending, and final consumer sentiment on Friday.

— news from S&P Global

— News Original —

Week Ahead Economic Preview: Week of 22 September 2025

The following is an extract from S&P Global Market Intelligence’s latest Week Ahead Economic Preview. For the full report, please click on the ‘Download Full Report’ link.

Download full report

Flash PMI surveys to provide insights into growth, jobs and inflation

Flash PMI survey data will provide a key focus for the markets in the coming week, though Friday’s release of the US core PCE price index will also be eagerly awaited. Other releases of note include revised US GDP numbers, consumer confidence data for the US and Europe, plus US, home sales, durable goods orders and inventories.

Early ‘flash’ PMI data will provide the first major snapshots of economic trends in September. Prior data showed especially strong growth in India accompanied by robust expansions in the US and Australia. More modest but strengthening upturns were meanwhile reported in the UK, Japan and – to a lesser extent – the eurozone.

A concern, however, is that some of the recent improvement in manufacturing growth globally has been fueled by the front-loading of shipments ahead of US tariffs. September’s factory PMIs will therefore be eyed to see if this boost is fading, and the extent to which rising domestic demand in economies such as Germany may be helping offset US trade issues. In France, the survey data will be eyed for the impact of political upheaval after the fall of the government, but in the UK the survey data will be important to gauge any ongoing impact of policy changes on both inflation and jobs. Higher employer tax and Minimum Wages have recently pushed up inflation and led to widespread UK job losses.

In the US, although the recent strength of the PMI’s current output index has bolstered the likelihood of the economy growing at a solid pace again in the third quarter, business confidence about the outlook has taken a knock, suggesting that that companies are becoming increasingly nervous about the outlook.

US PMI price data will also be eagerly awaited to assess tariff impacts. However, a further steer on the future path of US interest rates will also be provided on Friday by updated official inflation data. The publication of the Fed’s preferred measure of core PCE inflation follows mixed signals on recent price trends. While consumer price inflation picked up from 2.7% to 2.9% in August, wholesale prices showed a surprise 0.1% decline during the month. Softer inflation will likely be needed to open the door for further rate cuts in the months ahead. The last FOMC meeting, which saw the fed funds rate cut for the first time since December, showed policymakers were generally anticipating another two rate cuts by the end of the year, representing a more dovish stance than previously signalled.

Flash PMI surveys will be important to assess after recent data showed current output growth accelerating but confidence about future output deteriorating. Such a divergence is unusual, and the loss of optimism poses downside risks to the economic outlook.

Monday 22 Sep

Americas

– Canada PPI (Aug)

– US Chicago Fed National Activity Index (Aug)

EMEA

– Eurozone Consumer Confidence (Sep, flash)

APAC

– Hong Kong SAR Inflation (Aug)

Tuesday 23 Sep

Australia S&P Global Flash PMI, Manufacturing & Services*

India HSBC Flash PMI, Manufacturing & Services*

UK S&P Global Flash PMI, Manufacturing & Services*

Germany HCOB Flash PMI, Manufacturing & Services*

France HCOB Flash PMI, Manufacturing & Services*

eurozone HCOB Flash PMI, Manufacturing & Services*

US S&P Global Flash PMI* Manufacturing & Services*

Americas

– Canada New Housing Price Index (Aug)

– US Current Account (Q2)

– US Existing Home Sales (Aug)

EMEA

– Spain Balance of Trade (Jul)

APAC

Japan Market Holiday

– Malaysia Inflation (Aug)

– Singapore Inflation (Aug)

– Taiwan Export Orders (Aug)

Wednesday 24 Sep

Japan S&P Global Flash PMI, Manufacturing & Services*

Americas

– US New Home Sales (Aug)

EMEA

South Africa Market Holiday

– Germany Ifo Business Climate (Sep)

APAC

– South Korea Consumer Confidence (Sep)

– Australia Monthly CPI Indicator (Aug)

– Taiwan Industrial Production (Aug)

Thursday 25 Sep

Americas

– US Durable Goods Orders

– US GDP Growth (Q2, final)

– US Initial Jobless Claims

– US Wholesale Inventories (Aug)

EMEA

– Germany GfK Consumer Confidence (Oct)

– France Consumer Confidence (Sep)

– Switzerland SNB Interest Rate Decision

APAC

– Japan BOJ Monetary Policy Meeting Minutes (Jul)

– Thailand Balance of Trade (Aug)

– Taiwan Retail Sales (Aug)

– Hong Kong SAR Balance of Trade (Aug)

Friday 26 Sep

Americas

– Mexico Banxico Interest Rate Decision

– Mexico Balance of Trade (Aug n

– Canada GDP (Aug, prelim)

– US Core PCE Price Index (Aug)

– US Personal Income, Spending and Prices (Aug)

– US University of Michigan Consumer Sentiment (Sep, final)

EMEA

– Spain GDP (Q2, final)

– Italy Business Confidence (Sep)

APAC

– South Korea Business Confidence (Sep)

– Singapore Industrial Production (Aug)

– Thailand Industrial Production (Aug)

Download full report

© 2025, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers’ Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Learn more about PMI data

Request a demo

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.