The upcoming week promises a series of key economic releases that could shape monetary policy expectations across major economies. Investors and policymakers alike will be watching closely as data on employment, manufacturing activity, and inflation come into focus.

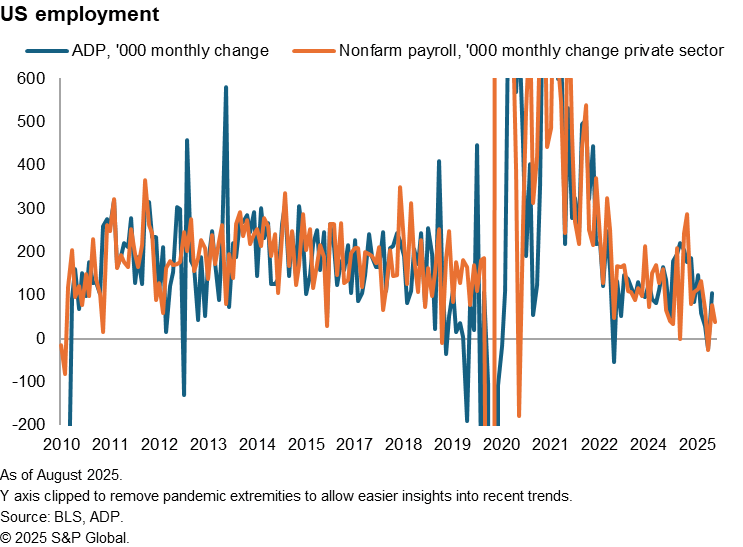

The U.S. nonfarm payrolls report for September will be a central highlight, potentially influencing the Federal Reserve’s stance on future interest rate adjustments. Although the Fed lowered rates by 25 basis points in September, officials including Chair Powell have emphasized that further easing is not guaranteed. Markets anticipate a modest addition of 39,000 jobs, following August’s 22,000 gain. While the unemployment rate is expected to remain steady at 4.3%, any signs of labor market deterioration could reinforce a dovish policy outlook.

Ahead of the official jobs report, several indicators will offer preliminary insights: the ADP private sector employment change, jobless claims, and JOLTS job openings data. These metrics will help assess whether the labor market is cooling in a sustained manner.

Global manufacturing conditions will also come under scrutiny through the release of flash Purchasing Managers’ Index (PMI) data. After reaching a 14-month high in August, global PMI readings suggest momentum may be fading. The initial boost from front-loaded trade activity ahead of U.S. tariff changes appears to be waning. Notably, U.S. input costs remain elevated due to tariffs, but selling prices have shown only moderate increases—indicating businesses are struggling to pass higher costs to consumers.

In Europe, flash estimates of eurozone inflation for September will be released alongside PMI figures. Both are expected to show inflation near the European Central Bank’s 2% target. Additional data on eurozone unemployment and UK mortgage approvals will provide further context on regional economic health.

In the Asia-Pacific region, central banks in India and Australia are expected to hold interest rates steady. The Reserve Bank of India is likely to maintain its current stance amid stronger-than-expected economic growth, while the Reserve Bank of Australia weighs persistent inflationary pressures.

A full schedule of economic events includes:

**Monday, September 29**

– Mexico unemployment rate (August)

– U.S. pending home sales (August)

– U.S. Dallas Fed manufacturing index (September)

– Spain inflation (September, preliminary)

– UK mortgage lending and approvals (August)

– Eurozone economic sentiment (September)

**Tuesday, September 30**

– Brazil unemployment rate (August)

– U.S. S&P/Case-Shiller home price index (July)

– U.S. JOLTS job openings (August)

– U.S. Conference Board consumer confidence (September)

– Germany retail sales and unemployment (August)

– France, Italy, and Germany inflation (September, preliminary)

– Japan industrial production, retail sales, and Bank of Japan summary of opinions (August)

– China’s NBS and Caixin manufacturing PMIs (September)

– Australia Reserve Bank interest rate decision

**Wednesday, October 1**

– Global manufacturing PMI (September)

– U.S. ADP employment change (September)

– U.S. ISM manufacturing PMI (September)

– Flash eurozone CPI (September)

– India Reserve Bank interest rate decision

**Thursday, October 2**

– U.S. initial jobless claims and factory orders (August)

– Switzerland, Spain, Italy, and eurozone unemployment data (August/September)

– South Korea and Indonesia inflation (September)

– Australia trade balance (August)

**Friday, October 3**

– Global services and composite PMIs (September)

– U.S. nonfarm payrolls, unemployment rate, and average hourly earnings (September)

– U.S. ISM services PMI (September)

– France industrial production (August)

– Turkey inflation (September)

– Japan unemployment rate (August)

– Singapore retail sales (August)

S&P Global Market Intelligence compiles PMI data for over 40 economies based on surveys of senior executives in the private sector. These indices offer insights into economic trends including GDP growth, inflation, employment, and exports, and are widely used by financial professionals for forecasting and strategic planning.

— news from S&P Global

— News Original —

Week Ahead Economic Preview: Week of 29 September 2025

The following is an extract from S&P Global Market Intelligence’s latest Week Ahead Economic Preview. For the full report, please click on the ‘Download Full Report’ link. n nDownload Full Report n nPayrolls and PMIs to provide new policy path clues n nUS nonfarm payrolls provide the crescendo to a busy week for economy watchers which includes worldwide manufacturing PMI surveys, flash eurozone inflation numbers and monetary policy decisions in India and Australia. n nThe monthly US employment report will provide guidance on the likelihood of further rate cuts this year. The Fed not only cut interest rates for the first time this year at its September FOMC meeting, but also revealed a general expectation among policymakers that rates could be cut another two times this year. However, officials including Fed Chair Powell have since sought to stress that the path to lower rates is by no means certain. Further signs of a weakening jobs market will therefore be important in maintaining a dovish stance. Markets are expecting just 39,000 jobs to have been added in September after the 22,000 gain reported in August. Such low numbers are thought to be consistent with rising unemployment, though there’s an expectation among analysts that the jobless rate will hold at 4.3% for now. The payroll report will be preceded by job openings (JOLTS) data, jobless claims and the ADP private sector job count to give some additional clues as to the labour market’s health. n nInsights into the global manufacturing economy’s health will meanwhile be provided by the worldwide PMI surveys. After August’s global PMI had hit a 14-month high, more recent flash PMI data have hinted at this performance losing steam as the boost to production and trade from the front-running of US tariffs fades. Besides these broader growth trends, developments on US factory prices will be key data to watch: September’s flash PMI numbers showed US input cost inflation remaining elevated due to tariffs, but selling price inflation moderated in one of the first signs from the survey that producers were struggling to pass these higher costs on to customers. n nIn Europe, the PMIs will be assessed alongside flash eurozone CPI inflation numbers for September, but both are likely to suggest inflation is still running at or close to the ECB’s 2% target. Also look out for eurozone unemployment data and UK mortgage approvals. n nIn APAC, central bank decisions in India and Australia are expected to see rates held steady as the former eyes faster than expected economic growth and the latter weighs up hotter than anticipated inflation. n nKey diary events n nMonday 29 Sep n nAmericas n n- Mexico Unemployment Rate (Aug) n n- US Pending Home Sales (Aug) n n- US Dallas Fed Manufacturing Index (Sep) n nEMEA n n- Spain Inflation (Sep, prelim) n n- UK Mortgage Lending and Approvals (Aug) n n- Eurozone Economic Sentiment (Sep) n n- Spain Business Confidence (Sep) n nAPAC n n- Taiwan Consumer Confidence (Sep) n n- Pakistan GDP (Q2) n n- India Industrial Production (Aug) n nTuesday 30 Sep n nAmericas n n- Brazil Unemployment Rate (Aug) n n- US S&P/Case-Shiller Home Price (Jul) n n- US JOLTS Job Openings (Aug) n n- US CB Consumer Confidence (Sep) n nEMEA n n- Germany Retail Sales (Aug) n n- UK Current Account (Q2) n n- France, Italy, Germany Inflation (Sep, prelim) n n- Germany Unemployment (Sep) n nAPAC n n- South Korea Industrial Production (Aug) n n- Japan BoJ Summary of Opinions (Sep) n n- Japan Industrial Production and Retail Sales (Aug) n n- China (Mainland) NBS PMI (Sep) n n- China (Mainland) RatingDog PMI* (Sep) n n- Australia RBA Interest Rate Decision n nWednesday 1 Oct n nWorldwide Manufacturing PMIs, incl. global PMI* (Sep) n nAmericas n n- US ADP Employment Change (Sep) n n- US ISM Manufacturing PMI (Sep) n nEMEA n n- UK Nationwide Housing Prices (Sep) n n- Eurozone Inflation (Sep, flash) n nAPAC n nChina (Mainland), Hong Kong SAR Market Holiday n n- Japan Tankan Index (Sep) n n- South Korea Trade (Sep) n n- Indonesia Inflation (Sep) n n- India RBI Interest Rate Decision n nThursday 2 Oct n nAmericas n n- US Initial Jobless Claims n n- US Factory Orders (Aug) n nEMEA n n- Switzerland Inflation (Sep) n n- Spain Unemployment Rate (Sep) n n- Italy Unemployment Rate (Aug) n n- Eurozone Unemployment Rate (Aug) n nAPAC n nChina (Mainland), India Market Holiday n n- South Korea Inflation (Sep) n n- Australia Trade (Aug) n n- Japan Consumer Confidence (Sep) n nFriday 3 Oct n nWorldwide Services, Composite PMIs, inc. global PMI* (Sep) n nGlobal Sector PMI* (Sep) n nAmericas n n- Brazil Industrial Production (Aug) n n- US Non-Farm Payrolls, Unemployment Rate, Average Hourly Earnings (Sep) n n- US ISM Services PMI (Sep) n nEMEA n n- France Industrial Production (Aug) n n- Turkey Inflation (Sep) n n- Italy Retail Sales (Aug) n nAPAC n nChina (Mainland), South Korea Market Holiday n n- Japan Unemployment Rate (Aug) n n- Singapore Retail Sales (Aug) n n* Access press releases of indices produced by S&P Global and relevant sponsors here. n nDownload Full Report n nPurchasing Managers’ Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities. n nLearn more about PMI data n nRequest a demo n nThis article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.