Global financial markets are preparing for the US Federal Reserve’s upcoming monetary policy announcement, with strong expectations of a 25-basis point rate cut. Despite rising inflation and solid business activity, weakening labor market indicators have increased pressure for monetary easing. The Federal Open Market Committee (FOMC) meeting is the centerpiece of this week’s economic calendar, even as policymakers remain divided on the path ahead.

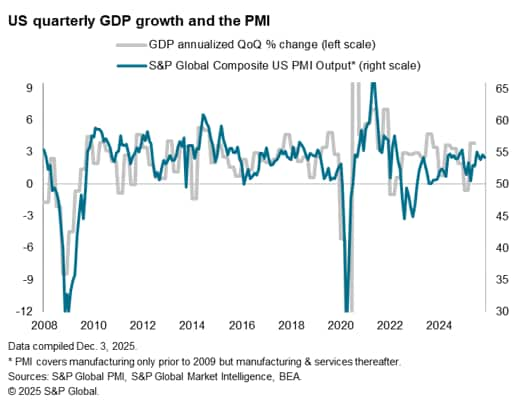

Recent data show US consumer price inflation climbed to 3.0% in September, and business surveys suggest ongoing inflationary pressures due to tariff impacts. At the same time, economic indicators such as the ISM and S&P Global PMI point to robust growth in the fourth quarter. However, signs of softening in the job market, including a decline in private sector employment reported by ADP, are bolstering the case for lower borrowing costs.

Market participants are closely watching the Fed’s updated economic projections for insights into future policy moves. Analysts forecast two additional 25-basis point reductions in 2026, with the first likely in June, contingent on clearer evidence of inflation moving toward target levels.

Outside the US, key releases include October GDP figures from the UK, which may rebound after September’s 0.1% contraction linked to a cyberattack-related shutdown at a major car plant. While manufacturing activity suggests some recovery, broader growth indicators remain subdued. Inflation data from mainland China and industrial output from Germany will also draw attention, alongside interest rate decisions in Canada, Brazil, Switzerland, Australia, Turkey, and the Philippines.

Investor sentiment in the US equity market will be gauged through the December Investment Manager Index (IMI), following November’s peak in risk appetite. Meanwhile, PMI surveys confirm continued expansion in the US economy, with November’s ISM data showing the strongest output increase since March, though employment metrics continue to deteriorate.

— news from S&P Global

— News Original —

Week Ahead Economic Preview: Week of 8 December 2025

The following is an extract from S&P Global Market Intelligence ‘s latest Week Ahead Economic Preview. For the full report, please click on the ‘Download Full Report ‘ link. n nDownload full report n nGlobal markets brace for US FOMC rates decision n nThe highlight of the coming week will be the US Federal Reserve ‘s monetary policy meeting, where a rate cut is widely anticipated. Key statistical releases include US job openings and employment cost data, monthly GDP numbers and the November recruitment industry survey results for the UK, plus inflation numbers from mainland China and industrial production for Germany. There are also interest rate decisions from Canada, Brazil, Switzerland, Australia, Turkey and the Philippines. n nDespite the November meeting seeing divisions among US policymakers on the FOMC, and Fed Chair Powell stating that “a further reduction in the policy rate is not a foregone conclusion — far from it”, markets are firmly pricing in a 25-basis point December rate cut. n nA rate cut would come despite US consumer price inflation having accelerated to 3.0% in September and despite concerns that the pass-through of tariffs could also exert further inflationary pressures, as indicated by business survey price gauges. Furthermore, business activity indicators, such as the ISM surveys and PMI from S&P Global, hint at robust fourth quarter GDP growth. However, the case for lower rates lies largely with the labour market, especially after the ADP payroll report signalled falling private sector jobs. n nWhile the current case for lower rates in December is by no means clear-cut, there is even greater uncertainty about the outlook for rates next year. Hence the markets will be particularly eager to assess the Fed ‘s revised forecasts and digest clues about appetite for any further loosening of policy in 2026. Our analysts expect two more 25 bps cuts in 2026 after the December cut, though with the first not occurring until June, as the FOMC awaits confirmation of an improving inflation picture. n nOur pick of the data releases is UK GDP for October. September ‘s data showed the economy shrinking by 0.1% in September, though this in part reflected the shutdown of the JLR car plant after a cyber attack. October should therefore see a car sector rebound, as signalled by the PMI, though the survey data suggest underlying economic growth remains close to stalled. n nInstitutional investment sentiment toward the US equity market will meanwhile be tracked through the December edition of the Investment Manager Index (IMI). November saw risk appetite at the highest so far this year. n nPMI surveys signalled a further robust expansion of the US economy in November. ISM data also indicated the sharpest upturn in output across goods and services since March. The survey data therefore point to underlying US GDP strength in Q4. However, employment indicators have been weakening. n nKey diary events n nMonday 8 Dec n nAmericas n n- US Consumer Inflation Expectations (Nov) n nEMEA n n- Germany Industrial Production (Oct) n n- Switzerland Consumer Confidence (Nov) n n- UK KPMG/REC Report on Jobs* (Nov) n nAPAC n nPhilippines Market Holiday n n- Japan GDP (Q3, final) n n- China (Mainland) Balance of Trade (Nov) n nTuesday 9 Dec n nS&P Global Investment Manager Index* (Dec) n nAmericas n n- Mexico Inflation (Nov) n n- US ADP Weekly Employment Change n n- US JOLTs Job Openings (Oct) n nEMEA n nUAE Market Holiday n n- Germany Balance of Trade (Oct) n n- UK Regional Growth Tracker* (Nov) n nAPAC n n- Australia NAB Business Confidence (Nov) n n- Australia Building Permits (Oct, final) n n- Philippines Industrial Production (Oct) n n- Australia RBA Interest Rate Decision n n- Taiwan Trade Balance (Nov) n nWednesday 10 Dec n nGEP Global Supply Chain Volatility Index* (Nov) n nAmericas n n- Brazil Inflation Rate (Nov) n n- Canada BoC Interest Rate Decision n n- US Wholesale Inventories (Oct) n n- US Employment Cost Index (Q3) n n- US FOMC Interest Rate Decision n n- Brazil BCB Interest Rate Decision n nEMEA n n- Norway Inflation (Nov) n n- Sweden GDP (Oct) n n- Türkiye Industrial Production (Oct) n n- Italy Industrial Production (Oct) n nAPAC n nThailand Market Holiday n n- South Korea Unemployment Rate (Nov) n n- Japan PPI (Nov) n n- China (Mainland) CPI, PPI (Nov) n nThursday 11 Dec n nAmericas n n- Brazil Retail Sales (Oct) n n- Canada Balance of Trade (Sep) n n- US PPI (Nov) n n- Brazil Business Confidence (Dec) n nEMEA n n- Sweden Inflation (Nov, final) n n- Switzerland SNB Interest Rate Decision n n- Türkiye TCMB Interest Rate Decision n nAPAC n n- Philippines BSP Interest Rate Decision n nFriday 12 Dec n nAmericas n nMexico Market Holiday n n- Mexico Industrial Production (Oct) n n- Canada Building Permits (Oct) n nEMEA n n- Germany Inflation (Nov, final) n n- UK Goods Trade Balance (Oct) n n- United Kingdom monthly GDP, incl. Manufacturing, Services and Construction Output (Oct) n n- France Inflation (Nov, final) n n- Spain Inflation (Nov, final) n nAPAC n n- Malaysia Industrial Production (Oct) n n- Japan Industrial Production (Oct, final) n n- India Inflation (Nov) n n- China (Mainland) M2, New Yuan Loans, Loan Growth (Nov) n nDownload full report n n© 2025, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited. n nPurchasing Managers ‘ Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities. n nLearn more about PMI data n nRequest a demo n nThis article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.