Colombia’s economy is showing signs of stabilization in 2025, emerging from an uneven recovery marked by structural constraints and global uncertainty. After post-pandemic volatility, activity has steadied, supported by resilient household consumption and selective sectoral strength. Real GDP expanded 2.4% year-on-year in the second quarter of 2025, driven by gains in entertainment, agriculture, and retail, while construction and mining continued to contract, highlighting the fragility of investment-led expansion. n nDomestic demand has been a central pillar of economic resilience. Consumer spending rose 3%, reflecting adaptability despite tight credit conditions. Investment grew modestly at 1.7%, with strong gains in machinery and equipment offset by a more than 10% drop in housing investment, underscoring persistent weakness in real estate. This contrast illustrates the economy’s reliance on capital goods for productivity amid ongoing bottlenecks in construction. n nInflation remains a pressing concern. After initial signs of moderation, price pressures reemerged, pushing headline inflation to 5.1% in August—well above the central bank’s 3% target. Food prices were the primary driver, while core inflation eased slightly, suggesting some relief from supply-side constraints. The Banco de la República has maintained its policy rate at 9.25%, prioritizing price stability over growth, and is unlikely to ease policy before year-end. n nLabor market conditions have improved gradually. Unemployment declined to 8.8%, and informal employment edged downward, though regulatory changes that raise labor costs could hinder formal job creation. External accounts show cautious optimism: Foreign currency inflows reached US$54.1 billion, supported by services and tourism, while goods exports stagnated and fuel shipments declined sharply. This shift reflects a slow but meaningful pivot toward agriculture and value-added sectors such as coffee and precious metals. The peso appreciated to 4,047 per US dollar, aided by lower risk premiums and growing investor confidence, though soft oil prices limited further gains. n nFiscal dynamics remain a vulnerability. The deficit is expected to exceed 7% of GDP in 2025, triggering the activation of the fiscal rule’s escape clause. A proposed tax reform aims to raise 26.3 trillion pesos (1.5% of GDP) through higher wealth and income taxes, surcharges on financial institutions, and the elimination of fuel-related VAT benefits. While essential for revenue mobilization, its passage faces political resistance and could dampen economic activity through higher fuel prices. n nLooking ahead to 2026, the outlook is cautiously optimistic. Growth is projected to accelerate slightly to 2.7%, supported by stronger performance in retail, financial, and insurance services, which are expected to grow 6.7% and surpass entertainment as the leading sector. Retail and professional services will maintain steady momentum, while information and communication may see a notable rebound. Inflation is forecast to ease to 3.7%, paving the way for gradual monetary easing and improved credit conditions. Exchange-rate stability is expected, with the peso hovering near 4,000 per dollar, while external accounts should benefit from continued strength in services and tourism. n nHowever, risks remain. Fiscal sustainability, global commodity volatility, and external shocks continue to pose challenges. Nevertheless, improving business sentiment and sectoral diversification are laying the foundation for sustained, albeit modest, growth. n— news from Deloitte

— News Original —

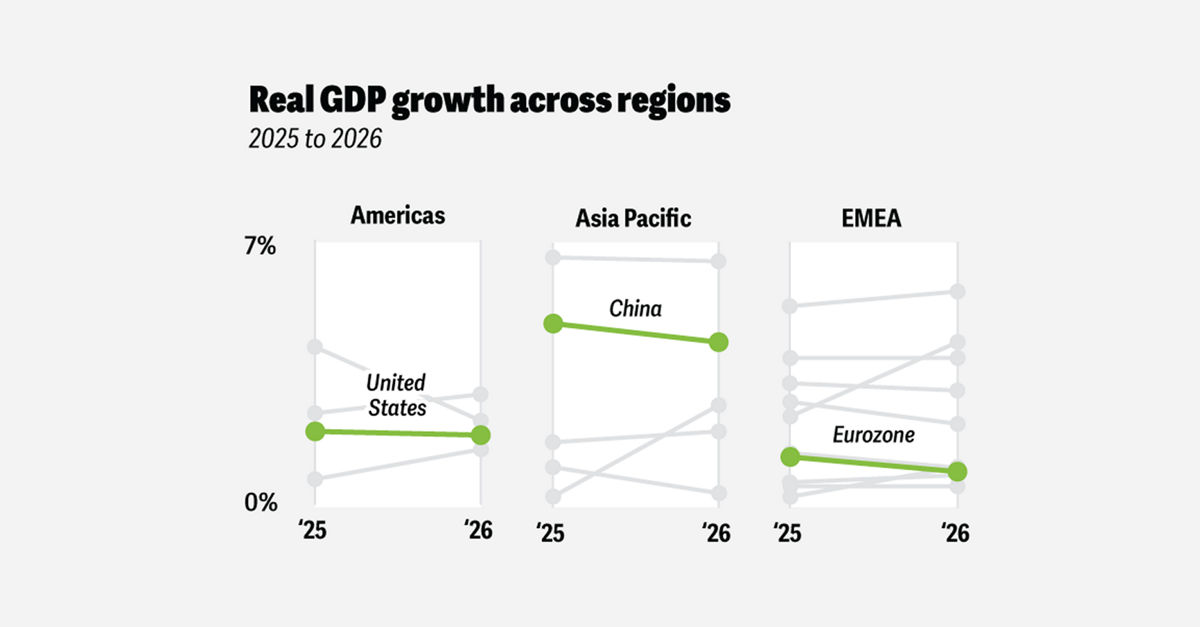

Global economic outlook 2026

Colombia n n– Daniel Zaga and Nicolás Barone n nThe Colombian economy is emerging from an uneven recovery, maintaining moderate growth despite persistent structural challenges and global uncertainty. After the pandemic, activity has stabilized, supported by resilient household consumption and selective sectoral dynamism. Real GDP grew 2.4% year on year8 in the second quarter of 2025, driven by entertainment, agriculture, and retail, while construction and mining continued to contract, underscoring the fragility of investment-led growth. n nDomestic demand has been a key anchor for Colombia. Consumer spending grew 3%,9 reflecting household adaptability even under tight credit conditions; investment, though positive at 1.7%, remains subdued, with machinery and equipment showing robust gains while housing investment plunged over 10%,10 signaling ongoing weakness in real estate. This divergence highlights the economy’s reliance on capital goods for productivity improvements amid structural bottlenecks in construction. n nInflation remains a primary challenge. After early signs of moderation, price pressures resurfaced, pushing headline inflation to 5.1% in August,11 well above the central bank’s 3% target. Food prices have been the main driver of inflation, while core inflation eased slightly, suggesting some relief from supply-side constraints. The Banco de la República has held its policy rate at 9.25%, prioritizing price stability over growth, and is unlikely to ease before year-end. n nLabor market conditions have improved gradually. Unemployment fell to 8.8%,12 and informality edged down, though regulatory changes increasing labor costs could slow formal job creation. Meanwhile, external accounts show cautious optimism: Foreign currency inflows reached US$54.1 billion,13 supported by services and tourism, while goods exports stagnated and fuel shipments declined sharply. This shift signals a slow but meaningful diversification toward agriculture and value-added sectors such as coffee and precious metals. The peso appreciated to 4,047 per US dollar, aided by lower risk premiums and investor confidence, though oil-price softness capped further gains.14 n nFiscal dynamics remain a weak link. The deficit is likely to exceed 7% of GDP in 2025, prompting activation of the fiscal rule’s escape clause. A proposed tax reform seeks to raise 26.3 trillion pesos (1.5% of GDP) through higher wealth and income taxes, surcharges on financial institutions, and the elimination of fuel-related value-added tax benefits. While critical for revenue mobilization, its approval faces political hurdles and could weigh on activity via higher fuel costs. n nLooking ahead, 2026 offers a cautiously optimistic outlook. Growth is projected to accelerate slightly to 2.7%, supported by stronger performance in the retail, financial, and insurance services sectors, which are expected to expand 6.7%, overtaking entertainment as the leading sector. Retail and professional services will maintain steady gains, while information and communication could see a notable rebound. Inflation is forecast to ease to 3.7%, paving the way for gradual monetary normalization and improved credit conditions. Exchange-rate stability is anticipated with the peso hovering near the 4,000 per dollar mark, while external accounts should benefit from continued momentum in services and tourism. n nBut risks persist. Fiscal sustainability, global commodity volatility, and external shocks remain key concerns for Colombia, although improving business confidence and sectoral diversification are creating a foundation for sustained, albeit modest, growth.