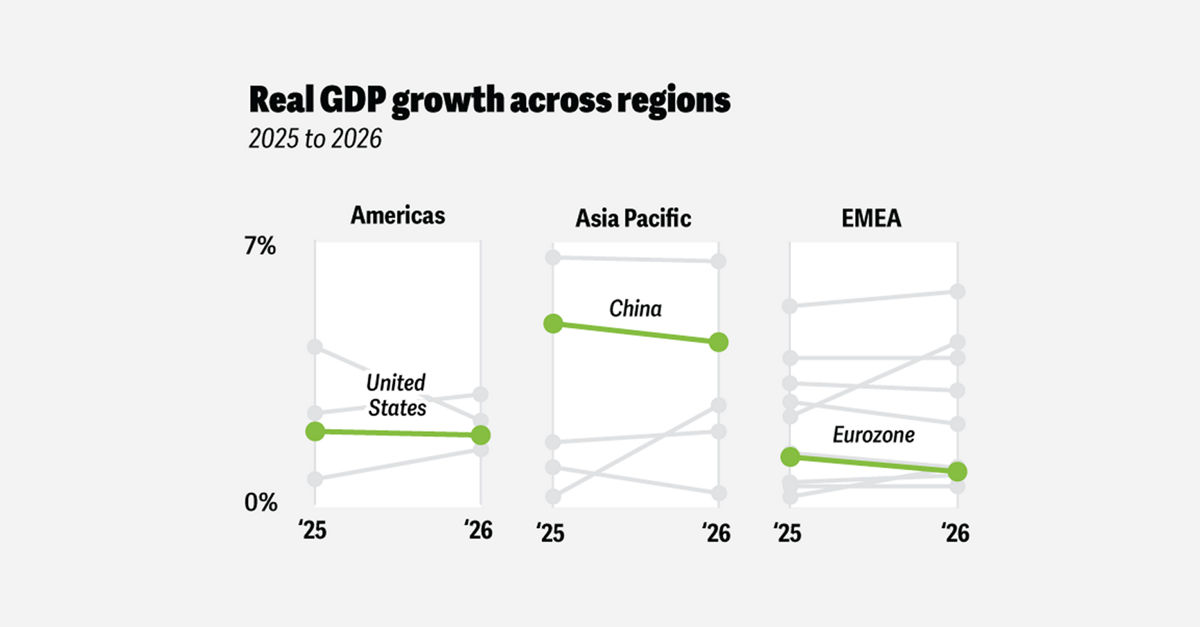

Italy’s economy experienced a slowdown in 2025, marked by very modest growth amid an unstable international environment shaped by escalating diplomatic and trade tensions. Exports of Italian goods outside the euro area declined, particularly in key “Made in Italy” industries such as food, leather goods, textiles, machinery, fashion, and jewelry—sectors that form the backbone of the national economy—due to higher tariffs and uncertainty over their enforcement. n nWhile construction showed mild expansion, activity weakened in services and most industrial sectors. Consumer spending stagnated, and the propensity to save increased. Despite high uncertainty stemming from evolving trade policies and ongoing conflicts, Italian GDP is projected to grow moderately in 2026 at 0.6%, with consumer price inflation expected to remain low at 1.5%—below the eurozone average. n nAfter a brief acceleration in the first quarter of 2025, GDP contracted from the second quarter onward, primarily due to a sharp drop in exports. Production growth lagged behind the eurozone average, with foreign trade volatility being the main driver of economic fluctuations. The imposition of U.S. tariffs and the euro’s appreciation against the dollar eroded competitiveness for European exporters. Italian firms, especially in the northeastern regions, faced growing export barriers. n nExport volumes declined from the second quarter of 2025, following a surge in the first three months driven by early shipments of maritime transport equipment ahead of tariff implementation. Goods exports fell most sharply outside the euro area, particularly to the United States, with notable drops in motor vehicles, food and beverages, textiles, clothing, and machinery. n nIn contrast, pharmaceutical exports expanded in 2025 due to exemptions from tariff hikes. Business sentiment among Italian exporters indicates rising concerns over trade barriers, margin pressure, and operational complexity, highlighting vulnerability to tariffs and geopolitical tensions beyond the European Free Trade Area. n nOn the supply side, the 2025 slowdown stemmed from weakness in services and parts of industry, partially offset by mild gains in construction linked to projects under the National Recovery and Resilience Plan (NRRP). Investment grew steadily in the first half of 2025, supported by corporate liquidity, declining interest rates, tax incentives, and early NRRP implementation. n nHousehold spending remained cautious throughout the year. Real disposable income grew faster than consumption, leading to higher savings. Employment stayed broadly stable, though labor force participation rose among older workers and declined among younger ones. Consumer decisions were supported by labor market resilience and expectations of low inflation, but the savings rate remained elevated compared to pre-pandemic levels. n nInflation in 2025 was higher than in 2024, as deflationary energy effects were offset by rising food prices and stronger service-sector inflation. For 2026, consumer prices are expected to decline and remain below eurozone levels. n nA growing concern is the economic impact of an aging population, particularly acute in Italy. This demographic trend poses risks to growth and public finances due to a shrinking workforce and potential productivity declines. Addressing this requires policies to boost labor participation and productivity, including greater digitalization and adoption of technologies like AI in high-value activities. Reducing the productivity gap between northern and southern regions—linked to institutional and infrastructure disparities—is another priority. n nResearch confirms a persistent efficiency divide across Italian regions. Meanwhile, studies suggest sports and physical activity can play a strategic economic role by improving health, social cohesion, and labor-force participation, thereby supporting GDP and employment. n— news from Deloitte

— News Original —

Global economic outlook 2026

Italy n n– Marco Vulpiani and Claudio Rossetti n nThe Italian economy continued to slow down in 2025, with very moderate growth. The year was characterized by an unstable international context, due to the deterioration of diplomatic and trade tensions. Italian goods exports contracted outside the euro area, especially to the United States and for the so-called “Made in Italy” industries (such as food, leather goods and textiles, mechanical products, fashion, and jewelry, which form the basis of the Italian economy), because of the effects of higher tariffs and uncertainty over their implementation. n nMoreover, a mild expansion in the construction sector contrasted with weakening activity in services and most industrial sectors. Consumption stagnated, and the propensity to save increased. Although future scenarios are subject to considerable uncertainty, stemming largely from potential new developments in trade policies and ongoing conflicts, Italian GDP is expected to grow moderately next year (0.6%), and consumer price inflation is expected to remain low (1.5%)56 and below levels expected in the euro area. n nAfter accelerating in the first quarter of 2025, Italian GDP contracted slightly from the second quarter onward, owing to a sharp decline in exports; production growth remained lower than in the euro area. This economic volatility is mainly attributable to foreign trade. In fact, the international context remained unstable throughout 2025. The imposition of US tariffs and the appreciation of the euro against the dollar are leading to a significant loss of competitiveness for European exporters. In this context, Italian companies are facing significant export obstacles, especially affecting the northeastern regions of the country and the “Made in Italy” sectors. n nItalian export volumes began to decline from the second quarter of 2025, following a sharp increase in the first three months of the year, mainly driven by sales of maritime transport equipment and a front-loading of trade before the new tariffs came into effect. Not surprisingly, goods exports contracted primarily outside the euro area, with the sharpest drop observed in exports to the United States because of the effects of higher tariffs and uncertainty over their implementation. The decline was especially marked for motor vehicles (subject to higher tariffs), food and beverages, textile and clothing products, and machinery. n nOn the contrary, exports of pharmaceuticals expanded in 2025, driven by the exemption of these products from tariff increases. Sentiment among Italian exporting companies57 also shows a growing perception of export barriers, rising pressure on margins, and increased operational complexity, suggesting a specific vulnerability to tariffs and geopolitical tensions outside the European Free Trade Area. n nOn the supply side, the cyclical weakening of GDP in 2025 is attributable both to services and to some industrial sectors, with a mild positive contribution from the construction sector due to projects under the National Recovery and Resilience Plan (NRRP). In the first half of 2025, investment continued growing at a sustained pace, supported by high liquidity reserves of firms, declining interest rates, the availability of tax incentives, and the implementation of a few NRRP measures. n nHousehold spending remained cautious throughout 2025, and real disposable income grew at slightly higher rates than consumption, translating into a strengthening of the propensity to save.58 Employment has remained broadly stable, while the participation rate has continued to rise among older workers and to decline among younger ones. Thus, households’ purchasing decisions are partly sustained by the resilience of the labor market and expectations of moderate inflation, but the propensity to save remains higher than it was before the pandemic. n nInflation was higher in 2025 than in the previous year. Deflationary pressures from the energy component were offset by increases in food prices and stronger growth in services. In 2026, consumer price inflation in Italy is expected to decline and remain below the levels expected in the euro area.59 n nAs a final note, there is growing concern about the economic consequences of an aging population—a phenomenon particularly notable in Italy. These include risks of slower economic growth and increased pressure on public finances. Slower growth can result from a shrinking workforce, which may also lead to lower productivity, requiring actions to sustain participation and labor productivity. For example, companies are required to increase the level of digital maturity of their business processes and to explore new technological opportunities (such as AI) to support worker productivity in high–value-added activities. Another area for strong improvement is the reduction of the geographical gap in productivity. n nResearch from the Deloitte Observatory on Italian regions confirms that a significant gap in productivity and efficiency between the north and the south of the country remains in most sectors of the economy, linked to persistent institutional and infrastructural differences. From another perspective, a Deloitte Italy economic research study60 shows that sport and sports practice, in addition to health, social, and behavioral benefits, also play a strategic role in the country’s economic development. Sports form a beneficial factor that can help counteract the aging of the population, capable of triggering large-scale economic and social benefits, such as increased productivity and higher labor-force participation, thus contributing to GDP and employment.